As states grapple with a host of contentious issues, including severe budget cuts, efforts to alter public employee rights and benefits, and legislation to curtail

Political candidates can be good for your nonprofit. They raise the profile of your events, increase public interest in your activities, and prove to be good friends once in office. Why

If you work for a nonprofit that aspires to have a nationwide or worldwide reach, it is likely you’ve spent some time thinking about the topic of local chapters.

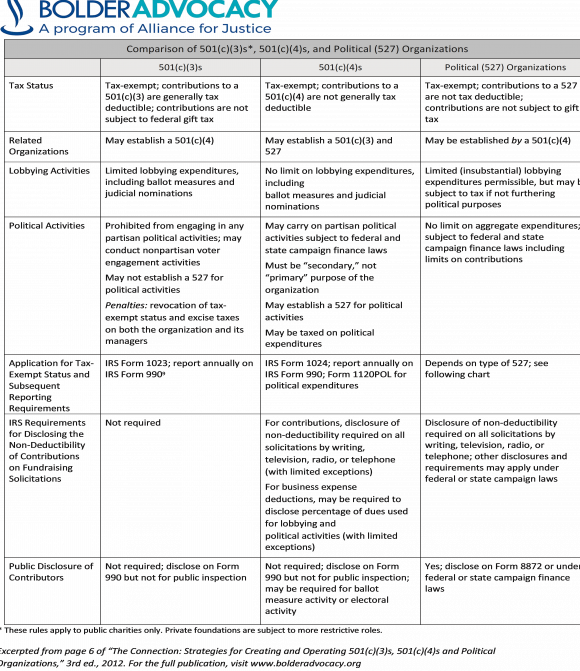

Nonprofits are allowed to lobby, but the type of nonprofit determines the level of lobbying allowed. Some nonprofits can engage in political activity, but not all are allowed that flexibility

The PATH Act (Protecting Americans from Tax Hikes Act) required that payments for services in 2017 be reported on Form 1099-MISC by January 31 of the following year. However, if a payor was o

An important part of outreach for many religious organizations are mission trips. It is an exciting opportunity for missioners to live into their faith by working in partnership with those th

While the Internal Revenue Code Section 501(c) lists 29 different types of nonprofit organizations, most tax-exempt organizations are those described in Section 501(c)(3) and have a charitable, rel

On December 29, 2022, President Biden signed the Consolidated Appropriations Act, 2023, which includes the provisions of the Securing a Strong Retirement Act, commonly called SECURE 2.0.

Special events, in this context, are synonymous with fundraising events such as galas (most typical), luncheons, golf tournaments, shows and auctions. They are unrelated to the exempt purpose

Whether or not this is the first time you are doing an auction or the auction is a regular event for your 501(c)(3) organization, this article will provide a variety of pointers which apply to live

In the first part of this two-part series, we discussed the growing commercialization of the non-profit sector, and examined how and when heavy reliance on “fee-for-service” revenue may be inconsis