Accounting and Bookkeeping

Depreciation

Once an item is recorded as a fixed asset, its life must be determined so depreciation can be calculated and recorded. Depreciation is the mechanism used to record the use of the item by the organization over its life until the value of the item is zero. Land and collectibles typically do not depreciate. The IRS has several guidelines on determining the life of a fixed asset and what method of depreciation to use.

Methods of Depreciation

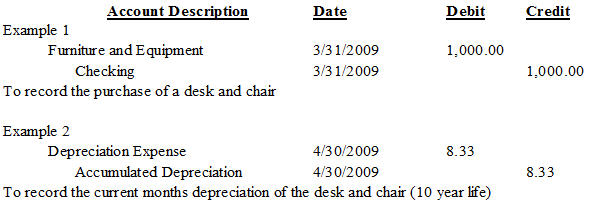

There are many methods of depreciation, but there is little reason for a nonprofit to use any method other than the straight line method. The straight line method works just like it sounds; the value of the fixed asset is depreciated evenly over the life of the asset. For example, an organization purchases a computer for $999.00 and determines its life to be three years. Each year $333.00 is recorded as depreciation. To do this, you debit the depreciation expense and credit accumulated depreciation. Accumulated depreciation is a negative asset account (referred by accounting professionals as a contra-asset account) used to capture depreciation and reduce the value of the fixed asset without altering the initial value recorded on the books under the furniture and equipment account.

Sample Journal Entries

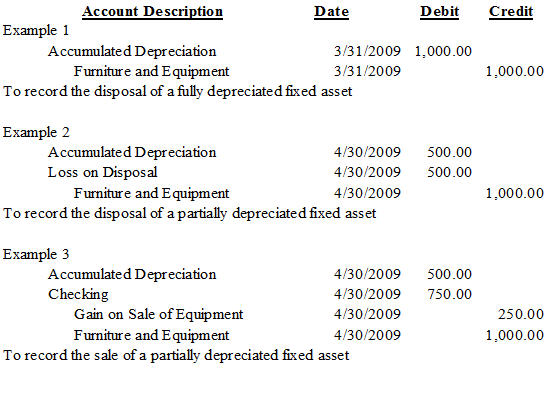

Disposal of Fixed Assets

When a fixed asset is disposed of or sold, it should be removed from the books of the organization. Below are examples of journal entries related to the disposal of fixed assets.