Subscribe to our newsletter

Can't Find Something? Ask Us

Nonprofit Accounting Basics

A good grants management process can take some time to develop, but the effort can be worth it. In this article, you’ll learn some tips and guidelines to help you improve your grants manageme

Often it is difficult to distinguish between a contribution and an exchange transaction, the following factors are indicative of an exchan

It may be hard to believe but getting too much money can sometimes destabilize a nonprofit organization.

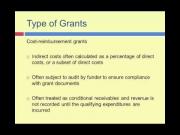

The following are the entries necessary for cost-reimbursable government grant (assuming the grant is determined to be an exchange transaction):