Nonprofit Accounting Basics

Common UBIT Myth Related to Nonprofit Revenue and Tax Impact

Myth: “It doesn’t matter how I get the money in the door as long as I spend it on charitable activities.”

Fact: The source of the revenue will determine whether it’s taxable income to the tax-exempt organization.

History: A 1950s cry for ending a macaroni monopoly at NYU created the starting point for the unrelated business income tax (UBIT) as we know it today. Hard to believe but true! Prior to congress approval of the law change, there was a “destination of income test” which meant that revenues could be earned tax-free by a tax-exempt entity no matter the source, so long as the destination of the income furthered the tax exempt’s purpose. In 1947, certain influential alumni donated their shares of ownership in the Mueller Pasta Co. to the New York University (NYU) School of Law, the former being a for-profit and the latter being a nonprofit. The controversy arose when for-profit competitors cried foul since NYU was earning tax-free income on the pasta maker’s commercial product. The response from the lawmakers led to the removal of the destination test and the addition of unrelated business income tax provisions. This change was widely viewed as creating parity or “leveling the playing field” between for-profits and nonprofits regarding business activities that were unrelated to the exempt purpose of the nonprofit.

Takeaway:

Tax-exempt organizations should review all revenue streams and document taxation implications for purposes of documentation under ASC 740 Uncertain Income Tax positions (the old FIN 48 that is still referenced on the Form 990 Part IV Line 11f).

- The standard here, as described in the typical financial statement footnote, is a greater than 50% standard, or more-likely-than-not, that the position taken for income tax will be upheld should it be put to the test of an IRS examination.

- Pro Tip: Be sure to analyze your organization’s miscellaneous revenue as well all other new and unusual sources of revenue.

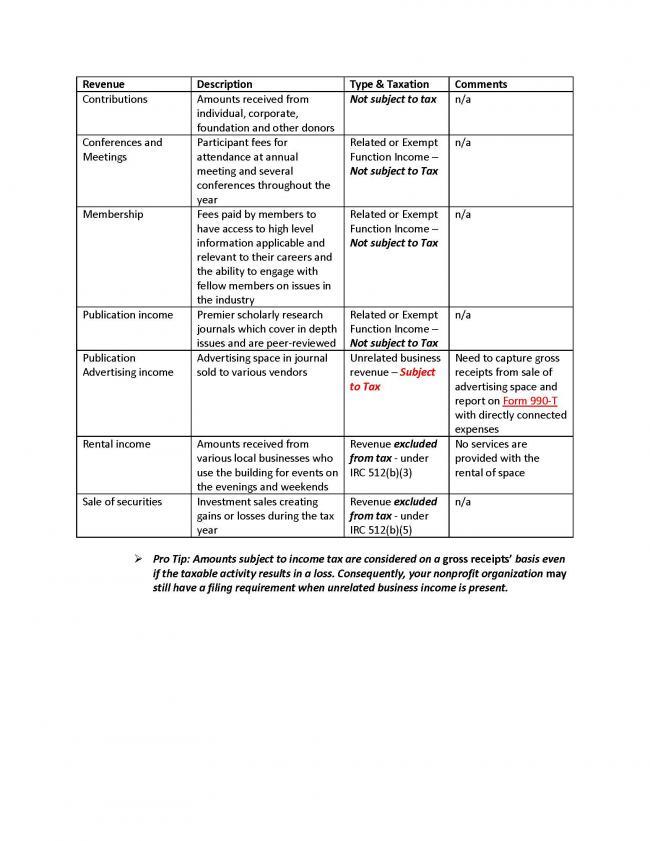

Show Me How: Here is a simple example that documents an organization’s oversight and determination of revenue streams income tax impacts for the applicable tax year: