About Us

Cash Flow-Internal Reporting

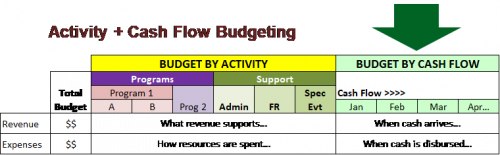

After allocating each line item across the organization’s mission and support activities, each line item should also be spread across the months of the fiscal year. To be truly useful, this should not be just a universal “divide by 12” exercise, especially for revenue line items.

An accrual budget can be adapted to estimate cash flow with some adjustments at the beginning and ending of a budget cycle to allow for the differences between the accrual budget and the timing of actual inflows and outflows of cash.

An accurate cash flow budget can serve as an early warning for tight months, allowing the board and staff to develop cash flow mitigation strategies such as reducing controllable expenses or planning to access a line of credit or funds from an operating reserve. Another action could be to take the cash flow projection to a supportive funder and request a change in the grant cycle timing to smooth out cash flow. Demonstrating this level of understanding and planning can build the funder’s confidence in the organization and help to enhance communications and deepen your relationships.

You may also be interested in Cash Flow Projections.