About Us

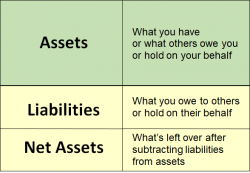

Liabilities

The Statement of Financial Position (SOFP) is the correct nonprofit term for the balance sheet. The SOFP comprises three sections: assets, liabilities, and net assets.

Liabilities are usually listed in declining order of their maturity. Current liabilities are those due within a year. Long-term liabilities are multi-year loans such as mortgages or other funds borrowed by the organization and payable over more than one year. Following are examples of what typically comprises liabilities for small and midsize organizations.

What you owe:

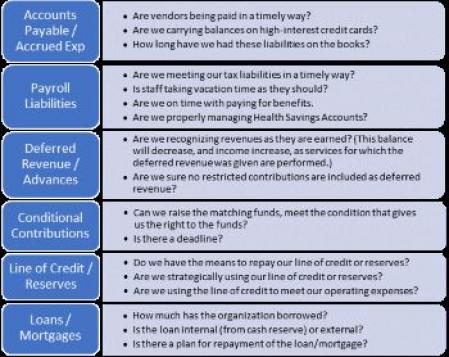

• Vendor accounts payable (bills for goods and services)

• Amounts payable on company credit cards

• Payroll liabilities (withholdings, federal, state, and local payroll taxes owed; unemployment owed, other benefits owed)

• Accrued expenses (sometimes estimated rather than based on actual bills, for instance: accrued vacation pay or accrued interest; can also include expenses related to the current period that were paid and expensed in a subsequent period)

• The amount accessed from a bank line of credit

• The inter-fund borrowing from a board-designated operating reserve

• Short-term or long-term loans, bonds payable, vehicle loans, mortgages, etc.

What you hold on behalf of others:

• Deferred revenue or refundable advances (funds paid to your organization in advance for services not yet delivered, considered liabilities since your organization would be liable to return these funds if the service is not delivered, for example, play subscriptions or tuition for future classes)

• Conditional contributions (funds given to your organization that you are entitled to only if the condition is met, such as a matching grant)

Liabilities are a natural “credit balance” meaning that, in an accounting entry, a credit to a liability account will increase it. A negative number (debit balance) in the liabilities section of the SOFP is not normal and should be questioned and explained.

Below are questions you might want to ask when looking at the liabilities balances to ensure that you understand the commitments your organization has made and when payments are due. This information is most helpful in trend, so looking at it in comparison to one or two previous fiscal years will help provide more context for your analysis of the data.

The answers to these questions, along with the answers pertaining to other SOFP sections, will provide a better understanding of the organization’s financial position.

Return to the Internal Reports Introduction page for links to greater detail on how to read various reports as well as recommended formatting.