About Us

The Statement of Functional Expenses

The Statement of Functional Expenses (SFE) is one of the standard reports within an organization’s audit. According to AICPA.org*:

“FASB [*] Accounting Standards Codification (ASC) Topic 958, Not-for-Profit Entities, requires all not-for-profit entities to present the relationship between functional expenses (such as major classes of program services and supporting activities) and natural expenses (such as salaries, rent, utilities, supplies, interest, and depreciation). For financial statement users, this analysis provides an in-depth look at how nonprofits spend toward their missions. For auditors and preparers, it necessitates consideration of the approach to the allocation and reporting of functional expenses.”

(*AICPA: Association of International Certified Professional Accountants, FASB: Financial Accounting Standards Board)

Internal Uses of Functional Allocation

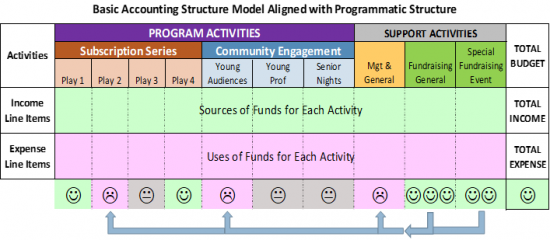

An organization must, at minimum, allocate expenses among program, management, and fundraising for purposes of the IRS 990 report and the organization’s audit (if applicable). Activity-based budgeting and reporting also benefits the organization as it allows an organization to see its business model. Internally, it makes sense to expand activity allocations to show income as well as expenses related to each activity showing which activities generate a surplus or require subsidy. See model illustration below. This report would more accurately be called a Statement of Activities by Class (function) or a Line Items by Activity Report.

Budgeting and reporting by functional activity, including the allocation of related/dedicated revenue, allows the staff, board, and other stakeholders to be aware of, and intentional about, how resources are used to accomplish mission and infrastructure activities. It also promotes analysis and discussion about the mission relevance of each activity in an organization’s program portfolio. These discussions can lead to renewed commitment for those program activities requiring subsidy and to exploration of different fundraising strategies to support them. Your reports can then tell you how close you are to your plan for each activity and whether you need to make any course corrections.

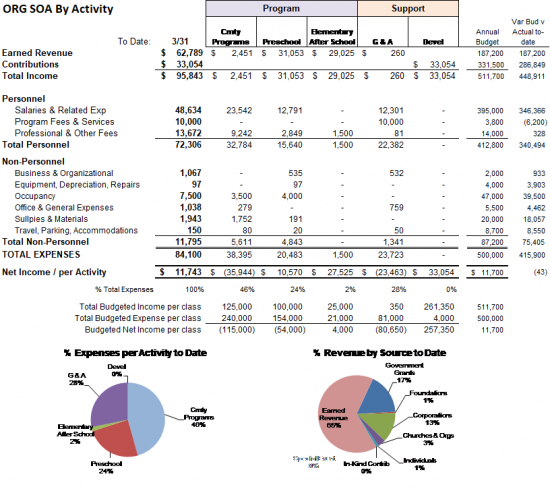

An expanded Statement of Functional Expenses, that is, a Statement of Activities (SOA) by Class (function) that includes related revenue, might look something like this for the first quarter:

This report model shows the year-to-date for each line item both in total and broken out by activity. The budget for each activity is shown at the bottom of each column. The reader can ask:

• What activities attract more than enough revenue to support themselves?

• What activities require subsidy? How much? How mission-relevant is the activity?

These data help to inform discussion and decisions regarding return on mission for programs.

In this report a reader can see that most programs, plus management, will require subsidy from contributions without restrictions (assigned to the Development activity). The organization is tracking on budget for net income, around $11,700, but individual activities are ahead or behind their net income targets at this point in the year.

Pie charts can be added at the bottom of the report to visually show the proportions of expense allocated per activity and the breakdown of revenue sources to-date and/or as budgeted. A column for year-end projections for line items can also be added. This report format is for internal purposes, as income is not shown in this manner in external reports.

Return to the Internal Reports Introduction page for links to greater detail on how to read various reports as well as recommended formatting.