About Us

Chart of Accounts-Net Assets

Net assets accounts reflect what is left over from assets after you subtract liabilities. “Net assets” is the nonprofit term or equivalent to for-profit equity or retained earnings. For small and midsize nonprofits without overly complex systems, 4-digit account numbers are usually adequate. Longer numbers can certainly be used, but that requires more keystrokes and may be harder to remember. Net assets account numbering usually begins with 3.

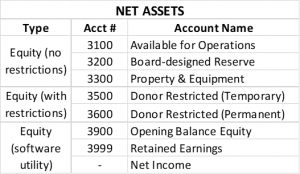

Here is a sample set of Net Assets accounts for a small to midsize organization:

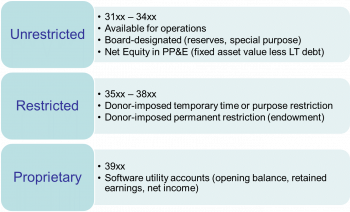

• Nets assets without donor restriction can be shown in order of liquidity.

• What is “available” for operations would be the most liquid.

• Funds can be set aside by the board for operating reserves or other special purposes, but they remain unrestricted as they can still be made available by board action.

• Net assets (equity in QB) in property, plant, and equipment (PP&E) comprises the value of net fixed assets (cost less accumulated depreciation) less any related long-term debt. This is the least liquid of unrestricted net assets and is not required.

• Net assets with donor restrictions can be time, purpose, or permanently restricted (i.e., endowment). The time or purpose restrictions are temporary, and these net assets can be released from restriction when the donor restriction has been met.

• An organization’s accounting software (e.g., QuickBooks) may have utility accounts in the net asset (equity) section.

o Opening balance equity is a startup holding account that should equal zero after the company setup has been accomplished. It should never have a balance after that.

o Net revenue (retained earnings in QB) accumulates the results of all prior year financial activity and current year net income reflects current year activity.

• An adjustment can be made to spread the balances from retained earnings and net income into the appropriate nonprofit net assets accounts. This procedure is discussed in another article , “Reclassing Net Assets in QuickBooks”.

Your accountant will know which of these accounts you actually need, and whether additional net assets accounts may need to be added. See also: Sample COA ~ Small-midsize Nonprofits .

© 2021 Elizabeth Hamilton Foley

This information is provided for small and midsize nonprofit organizations for educational purposes only. It is not comprehensive and should not be considered legal or accounting advice on any specific matter. The user of this template/sample is responsible for tailoring the contents to meet the specific needs and circumstances of the organization.