About Us

Chart of Accounts-Revenue

Operating revenue may derive from two broad categories: 1) earned (or exchange transactions), usually from program activities or contracted services or from investments, and 2) contributions, usually in the form of gifts, grants, or in-kind goods or services from institutions, agencies, or individuals. Contributions may also come with donor restrictions that are either temporary (time or purpose) or permanent (endowment). Contributions with restrictions can be temporary in nature and may be released from restriction to become operating revenue, but it should be recorded separately from operating revenue until it is released.

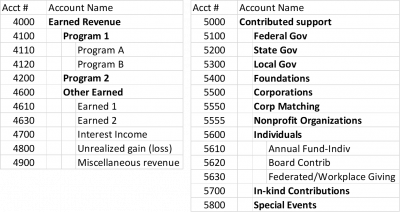

Operating Revenue Accounts

For small and midsize nonprofits without overly complex systems, 4-digit account numbers are usually adequate. Longer numbers can certainly be used, but that requires more keystrokes and may be harder to remember. Operating revenue account numbering usually begins with 4 and 5, with the 4-thousands indicating earned, and the 5-thousands contributed, or vice versa; there is no rule as to whether earned revenue or contributions should be shown first. If an organization has an appreciable amount of program-related earned revenue, it may choose to show earned revenue before contributions to give prominence to the mission activity that attracts the earned revenue; significant earned revenue directly from the organization’s constituency may serve as a validation of the success of its programs.

Revenue accounts should clearly identify the sources of revenue. Why? Typically, there is a different resource development strategy for raising revenue from various sources. The marketing and fundraising staff and board resource development committee would want to know your progress toward meeting your goal (budget) for each source. At the very least, you will want to track earned revenue separately from contributions, if for no other reason than to facilitate completion of the IRS 990 information return.

Below is a sample set of earned operating revenue and contribution accounts for a small or midsize organization. The program revenue accounts will need to be customized to reflect the appropriate revenue sources for your organization, using further sub accounts as necessary.

Earned revenue can be sub-divided into program revenue (contracts and fees for service, ticket sales, tuition, publication or program merchandise sales, rentals, etc.) vs. “other” earned revenue (concessions, advertising, non-program rentals, interest, and miscellaneous income).

Contributions are best shown by source. I’ve seen groups create a new income account for each government agency, foundation, or corporation that gives them money, by name, but it is more appropriate to use the accounting software’s customer / donor naming capability for that purpose. Constantly adding new accounts will result in a cluttered and unwieldy accounting system and overly lengthy and/or inconsistent report layouts.

Other Revenue Accounts

Some accounting software systems allow for “other revenue” and “other expense” type accounts to be created. These are especially useful to segregate activity from contributions with donor restrictions from contributions without donor restrictions, and capital expenses from “ordinary” expenses.

The following “other revenue” type accounts can be set up for tracking restricted grants. Other revenue accounts would be numbered in the 8-thousands.

Here, the 8100 account is a header with contributions with donor restriction subaccounts, followed by a “contra” account (8199). The contra account is used to release assets from restriction via journal entry. The 8199 account is debited, and the other half of the entry credits the income to its natural income source category (e.g., 5400-Foundations from the above list). That released revenue will then cover the expenses intended by the grant in the period during which those expenses happened. The total for “Restricted Activity” will show the net between the increases and the releases during the fiscal year.

The release entry for purpose restricted grants would continue to be tagged (assigned) to the name of the donor, as would the expenses the grant covers, so that a grant report can be setup and memorized in the accounting software to track the use of the grant.

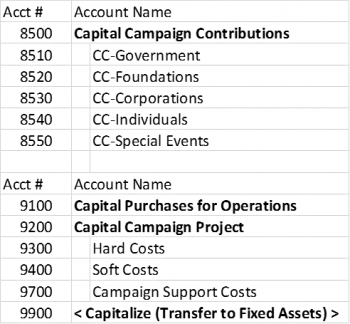

Contributions toward a capital campaign would best be tracked separately from restricted net assets that will ultimately support operations when released.

<< This is a set of capital campaign (CC) accounts, again allowing the organization to track campaign income by source.

You may want to add a CC contra account for releases of campaign revenue to cover capital costs.

Your accountant will know which of these accounts you actually need, and whether additional income accounts may need to be added. See also: Sample COA ~ Small-midsize Nonprofits .

© 2021 Elizabeth Hamilton Foley

This information is provided for small and midsize nonprofit organizations for educational purposes only. It is not comprehensive and should not be considered legal or accounting advice on any specific matter. The user of this template/sample is responsible for tailoring the contents to meet the specific needs and circumstances of the organization.